The region of Europe is characterized by the diversity of its national social security systems, as well as by the scale and scope of the coverage these provide.

Regardless, all the region’s social security systems are confronted by the challenges associated with population ageing. Across the region, countries are at different stages of the demographic transition. Some are at a very advanced stage, including Czechia, Germany, Hungary, Italy and Spain. These countries’ population profiles are among the oldest in the world. By contrast, other countries, such as France and Ireland, have relatively young profiles, as do certain parts of the Russian Federation. To respond to the process of population ageing and to cope with the evolving needs of populations, existing health and retirement systems require to be adapted.

As regards old-age income security, the region’s countries typically operate social insurance old‑age pension systems alongside the provision of tax-financed benefits, with countries allotting a greater or lesser role to mandatory or voluntary private retirement savings. For all countries, there will be a need for higher expenditure over the medium and long term to respond effectively to population ageing. Although population ageing is a global phenomenon, the region of Europe presents a distinctive picture. In most countries, the process of population ageing is long‑standing and very advanced. For other countries, it is more recent, and the transition may occur more rapidly. Irrespective of the national institutional model, country responses must involve reforming the existing systems used to manage old-age income security and health risks and developing new policy responses to meet elders’ needs. Faced with these challenges, ISSA member organizations are developing innovative policies that aim to respond to population ageing, including specific measures promoting the introduction of professional support services for people who have lost a degree of autonomy and solutions that are accessible to the oldest and most vulnerable.

Key messages

- The region of Europe is characterized by a diversity and multiplicity of institutional regimes and by demographic profiles which, despite variations, all exhibit the trends associated with population ageing.

- Population ageing is most advanced among the region’s richer economies but is underway across the entire region. The pace of ageing is more rapid in the region’s less advanced economies where budgetary resources may be limited to cope with this policy challenge.

- Ongoing efforts to ensure pension system financial sustainability in response to population ageing have led to less generous pensions in most countries, with a reduction in rights. Effective retirement ages have risen by two years on average compared to the 1990s and projections suggest an additional rise of four years will be necessary by 2070. The reduction of rights and increased contributions resulting from reforms may lead to a greater polarization of income among the elderly.

- Despite increases in the activity rate, the size of the region’s active population will shrink, especially if net migration levels decline. The total population will decrease, especially after 2035, while the number of people aged 65+, as well as aged 80+, will increase significantly. These factors will act to reduce system revenue and increase expenditure, especially for health care.

- Population ageing necessitates the development of formalized long-term care and services. The professionalization of these services is essential.

- To respond to population ageing, ISSA member organizations in the region have i) developed and reinforced policies to formalize caregiving to ensure the viability of the necessary services and the mobilization of all available resources; ii), implemented solutions to meet the needs of the elderly; and iii) strengthened the resilience of the services provided, most recently in the context of the pandemic, often through the deployment of new technologies.

Facts & trends

Characteristics of population ageing

The Madrid Plan of Action, adopted at the Second World Assembly on Ageing in April 2002, recognized ageing as a global phenomenon. This policy challenge also influences part of the United Nations Sustainable Development Goals, to create an inclusive society for all ages. On this basis, all countries report annually on progress achieved towards the Sustainable Development Goals, such as reducing poverty and inequality and improving health protection (UN, 2020). During the World Health Assembly in May 2016, 194 countries, including almost every State in the region, recognized the need for a national long-term care system. At the subregional level, the European Union monitors ageing in its Member States, and supervises budgetary variations in this area (European Commission, 2020).

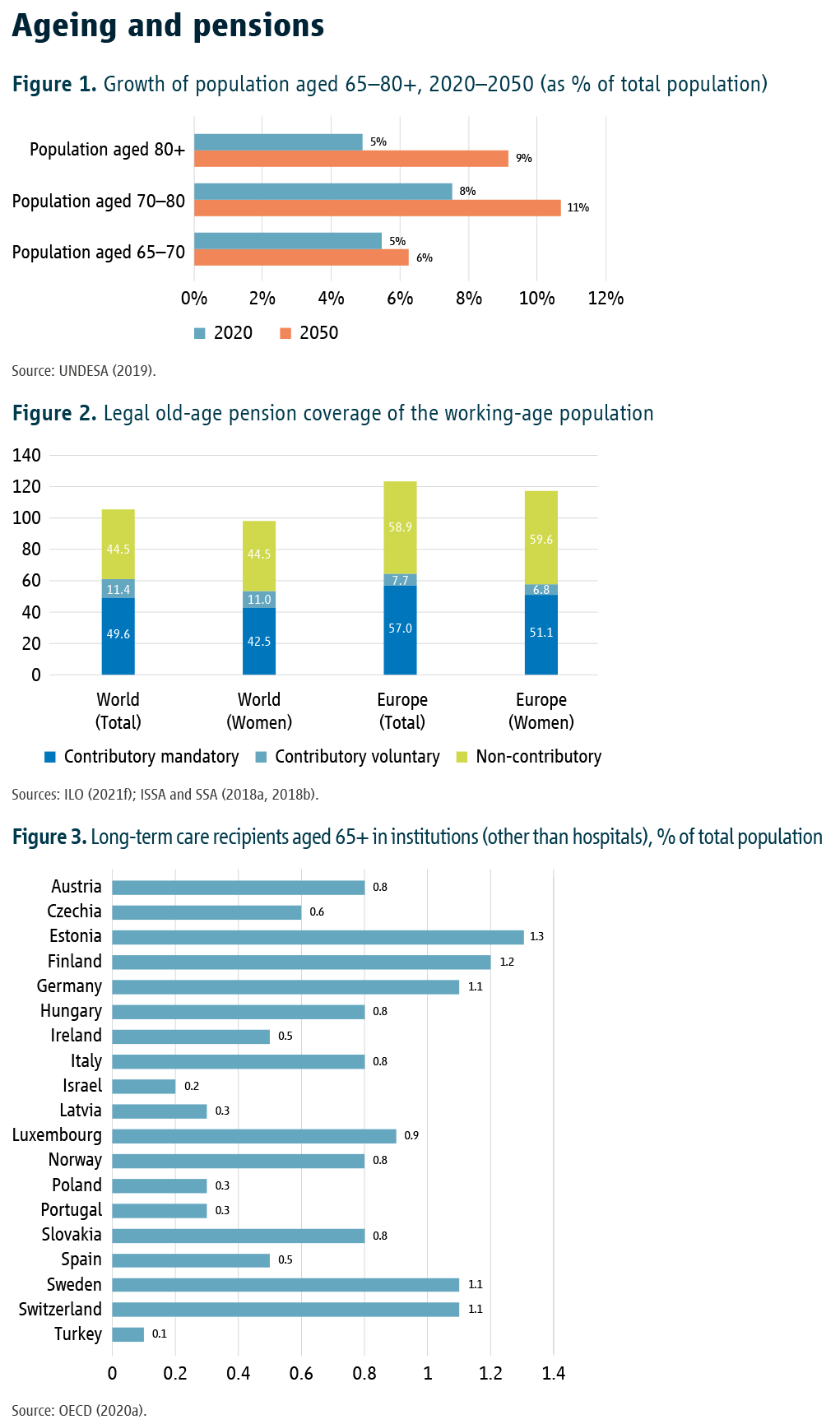

Globally, population ageing is currently more advanced in the industrialized countries. For the region of Europe this is most notable among countries of South, Central and Eastern Europe. An adequate level of economic and institutional development is an important prerequisite for dealing with the phenomenon of ageing in an effective manner. By 2050, Europe will be the global region with the highest proportion of elderly citizens in the world. Currently, 20 per cent of the region’s population is aged 65+; by 2070, it is projected to reach 30 per cent. At the same time, the proportion of people aged 80+ is expected to more than double, reaching 13 per cent of the total population by 2070.

The ageing of the population will also have consequences for morbidity profiles: infectious diseases are on the wane, but longterm non-contagious conditions such as cardiovascular diseases, respiratory syndromes, hyperglycemia, high cholesterol and cancer are increasing. This rise in chronic disease leads to a greater vulnerability to epidemics, such as the current COVID-19 pandemic, which is particularly dangerous for people aged 65+.

In the long term, with demographic renewal no longer guaranteed, the region’s population is expected to decrease by 5 per cent, yet the share of those aged 65+ will increase. As a result, the demographic dependency ratio (the ratio of the number of dependent people to those of active working age) should rise from 35 per cent to 60 per cent. These averages conceal considerable disparities within Europe – by 2070, the ratio may range from less than 30 per cent in certain Russian provinces to 90 per cent in Poland – but illustrate the widespread nature of the phenomenon (Gletel-Basten et al., 2017). As a result, the region’s workforce is projected to shrink by an average of 16 per cent by 2070.

In the immediate term, the fall in the birth rate, which is particularly pronounced in the south and east of the region, and the increase in life expectancy are leading many countries in Europe into a period of “pronounced ageing”, wherein the share in the population of dependent people (children and the elderly who are no longer able to work) is rising faster than that of economically active people (workers).

Differences in national profiles reflected in differing care approaches

Different models for the financing of old-age social protection are found in the region. As regards retirement, the dominant model in the region is the pay-as-you-go pension system. These pensions are financed by social security contributions averaging around 21 per cent of salary and are usually accompanied by tax-financed universal benefits. This is the system in Belgium or France, for example. Denmark, the Netherlands and the United Kingdom, are among countries that have a system of universal pensions that base eligibility on a minimum residence condition, and which are supplemented by a capitalization system, often using a defined contribution financing model. Some countries, such as Poland or Sweden and to a lesser extent Germany, have initiated a transition towards general defined contribution pension systems (notional or individual), often partially funded. Other countries in Europe, particularly in the southeast of the region, operate an alternative approach that combines a universal state system with a provident fund, permitting lump-sum benefits to be paid out at different times in the life course. This typology of retirement provision has not stabilized, with many countries in the region having shifted the distribution of the cost burden between the first two “pillars” during the 2010s in favour of the first. Some have introduced redistributive measures to compensate, at least in part, for the shortcomings of private retirement savings schemes in terms of their levels of coverage or adequacy. Hungary, Poland and the Russian Federation being notable examples in this regard.

Regardless of national profile, the measures taken to ensure the general sustainability of pension systems can be summed up under four main approaches (Dumont, 2020): i) compressing or reducing the financial value of the pensions paid to retirees; ii) increasing the deductions payable by working people (either higher contributions for pay-as-you-go pensions, or lower interest and dividends paid to individual capitalization accounts); iii) increasing the size of the active working‑age population; iv) public borrowing to finance pensions, which amounts to a higher financial burden for future generations of workers and taxpayers. Countries in the region are faced with the need to ensure the financial equilibrium of pension systems. This entails taking into account projections of the future number of pensioners, the average number of years spent in retirement and the number of people creating wealth. Countries in the region have used all means available to increase contributions, shift a degree of responsibility for ensuring income security in old age onto individuals, increase the activity rate among older people, and delay the effective retirement age. Policies to encourage active ageing have borne fruit: the activity rate among the cohort aged 55–65, especially women, has risen by 10 points, while the average age of effective retirement has risen by 2 years since 1990 (but will need to rise by a further 4 years by 2070). Nevertheless, these changes will not be sufficient to offset the net decline in the size of the working population. It should be noted that the Russian Federation is an exception here (Nadirova, 2018) – having one of the highest activity rates among older people in the region, it has not implemented reforms seeking to increase it (Galina et al., 2018).

In total, the net cost of ageing is projected to increase by 1–2 per cent of the region’s GDP by 2070. This is despite the tightening of the rules for calculating retirement pensions. Significantly, this increase is mainly due to a growth in age-related health expenditure.

All health care systems face high expenditure needs. Simply put, increasing longevity without any corresponding change in profiles will lead to a widespread increase in costs over people’s lifetimes, including for general health expenditure (Breyer, Costa-Font and Felder, 2010). When the costs associated with advances in medical care and the need for highly qualified professionals are factored in, expenditure will also rise – it is estimated that this accounts for 50 per cent of the growth in health expenditure since 1980 (Willemé and Dumont, 2015). As discussed, the future number of active contributors is expected to decrease. In turn, the financing challenge increases as the role of out-of-pocket health spending declines vis-à-vis collective health insurance: in emerging European economies individual health-care expenditure still represents an average of 30 per cent of total health expenditure, compared with 10 per cent in Western European and Scandinavian countries. In addition, over the past three decades, many countries in the region have introduced a system of universal coverage.

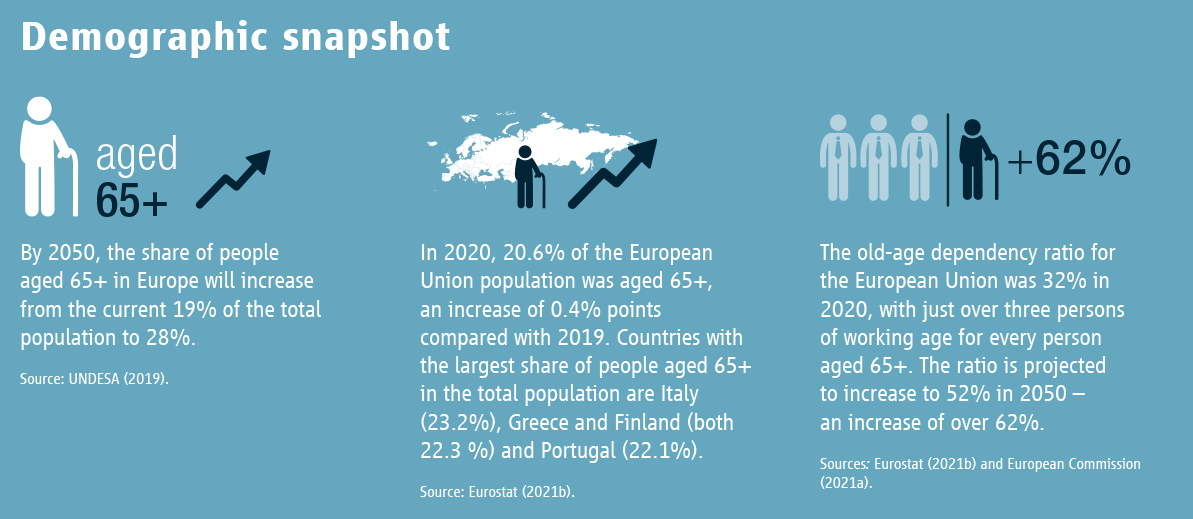

Faced with the challenges ahead, addressing the issue of the informal economy remains essential for the financing of appropriate institutional schemes. This is particularly true in the case of long-term retirement benefits or for measures to support independent living for the elderly, for which stable and regular financing is necessary. Although this too varies from one country to another, the size of the informal economy constitutes an additional hurdle to overcome concerning institutions’ ability to respond well to population ageing. Concerning these challenges, there is an important gender dimension. A concern about ineffective or insufficient contribution collection is particularly significant in countries where the income security of the elderly is mainly derived from universal public pension systems. In practice, basic universal pension systems financed by taxation are ultimately responsible for much of the response to ageing, while the benefits of retirement savings schemes, which are often tax-subsidized, remain the privilege of a better-off minority.

The polarization of retirement income is a phenomenon found in all countries, including those that have increased pension contributions to ensure the financial sustainability of their pension systems. In Sweden, for example, the average worker can expect a gross replacement rate of 55 per cent of average income from his or her entire working life, whereas a worker whose remuneration was twice the average can expect a replacement rate of almost 140 per cent. For the latter, they will receive a pension almost six times greater than that of the median worker (OECD, 2021). The same phenomenon is observed in those countries where the role played in national retirement systems by private pension funds is more important, such as the United Kingdom, Denmark and the Netherlands.

Retirement and health systems are having to deal with the new needs resulting from pronounced ageing. One of the difficulties is how to differentiate between care services, financed by health insurance, and social support. The ability to carry out activities of daily living (ADLs: eating, bathing, dressing, toileting, mobility, and continence) is generally used as a key indicator to assess the need for care, on the one hand, and for support services, on the other hand. It is entirely possible to need support services, but not care, to perform these six ADLs. The qualification level (and the unit cost) for providing such support is lower than for care services that require qualified medical personnel.

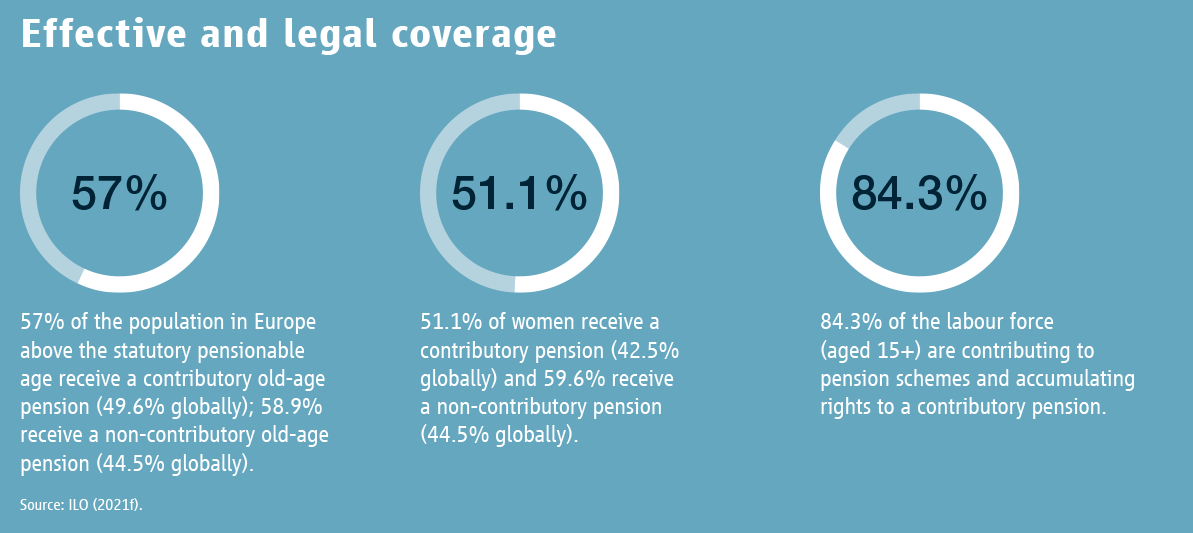

Several countries in the region have introduced a system of longterm care insurance (LTCI) to help people pay for regular care received at home or in an institutional setting. In this regard, equal access to rights is a challenge. For example, in 1995 Germany introduced LTC for the elderly using a social insurance financing mechanism, with the aim of ensuring equal rights. In Belgium, LTC consists of a wide range of services organized primarily at regional and municipal level and shows strong disparities from area to area. France, meanwhile, has established a so‑called “fifth social security risk”, the uniform response to which is provided by local authorities, supported by a national compensation fund to ensure equal LTC treatment throughout the country.

To reduce gaps in the care pathway and avoid unnecessary hospitalization, it is necessary to ensure coordinated services and care, enabling elderly people to stay at home for as long as possible. In recent years, several countries have adopted a more comprehensive approach to providing long-term care and services to older people and facilitating “ageing in place”. In 2009, the Netherlands inaugurated “Hogeweyk”, a pioneering care facility for older people with dementia, which focuses on ageing in place and quality LTC. The establishment is referred to as a “village” rather than a “hospital”, and its inhabitants are called residents rather than patients. The evolving nature of such innovative policies involves additional financial inputs. Cash benefits, which may be less costly, such as financial incentives for non-professional carers (or carers without professional status) can sometimes be provided, for example in the United Kingdom, Ireland, Italy and Denmark. Such benefits recognize that “informal carers” play a major role in the proper functioning of LTC systems in Europe. In ageing societies, however, it makes sense to foster a professional workforce to allow carers to take leave breaks and to receive training in a sector that is likely to rely heavily on immigrant workers (Bornia et al., 2011).

The use of new ICT is being developed to provide optimal assistance to the elderly. In Germany, research into outpatient, informal and cross-sectoral care is also exploring the potential of digital technology to improve the independence of care recipients and relieve the pressure on formal and informal carers. In Austria, a policy has been put in place to facilitate Internet training for the elderly (Firgo and Famira-Mühlberger, 2020).

Whatever form the institutional organization of the pension and health systems takes, the organization of vocational education and training and the formalization of the framework of support activities for the elderly constitute key elements in an appropriate response to the new financial organizational challenges of ageing. This is particularly true for the financing of policies to support elders to remain independent, the implementation of which will be one key budgetary challenge for the years to come (Safonov and Shkrebelo, 2021). In addition to supporting the formalization of work and professional development for carers there is a need for institutional support for informal carers (Muir, 2017), such as family members or people in the local community, whose involvement has been shown to be important to ensuring elderly well-being and their independent living (Varlamova et al., 2020). The introduction of professional caregiving standards is essential to avoid any form of mistreatment of the elderly.

Initial institutional responses

Framed by three main policy objectives, various operational solutions have been put in place to meet the challenges presented by population ageing.

First, there is a need to ensure the introduction of services for an ageing population. To improve services for workers approaching retirement as well as the retired and elderly, especially those who require care at home or in an institution, various initiatives have emerged. The Swedish Pensions Agency (SPA) has set up a retirement planning tool (Uttagsplaneraren) that citizens use to assess the impact on their pension income of decisions concerning their choice of retirement age. To meet the needs of older people and help them to remain independent, various countries have implemented policies. For example, in Azerbaijan, where the Agency for Sustainable and Operational Social Security (DOST) operates a policy that aims to support isolated elderly people with the activities of daily life. To improve the support given to families in difficulties, Poland’s Social Insurance Institution (ZUS) has implemented exceptional services that are also intended for the elderly as part of a so-called “anti-crisis shield” policy.

Second, it is essential to safeguard the resilience of services for elders even in times of a political, social or a public health crisis. As regards the resilience of dedicated services, various solutions have been developed. To maintain services that have been seriously affected by the COVID-19 pandemic, specific protocols have been introduced that make extensive use of ICT. For example, Finland’s Social Insurance Institution (KELA) has deployed two chatbots (Kela‑Kelpo and FPA‑Folke) to assist insured persons, particularly in the context of the pandemic. A further example is the possibility, introduced by Poland’s ZUS and elsewhere in the region, of organizing virtual visits and meeting advisers by video link. Numerous remote services provide personalized guidance for insured persons, regardless of time and place. Widespread use has been made of digital tools to allow contactless access to all the services offered. For example, Germany’s Federal Pension Insurance (Deutsche Rentenversicherung Bund – DRV) has implemented a major digital strategy. Such a development requires the roll-out of support and training services for the use of these new tools, especially for the elderly, who may be more reluctant to use such technology. Latvia’s State Social Insurance Agency (SSIA) has deployed, through the unified customer service provided by local authorities, computer trainers (e‑assistants) to familiarize users with online services.

Third, it is necessary to strengthen the formalization of the labour market and extend social protection coverage. Improvements in access to formal employment, which will widen the contribution and tax base, will strengthen the public financing of services and support for the elderly (ILO, 2021b). In this regard, various approaches are being developed across the region. Public education concerning the role of social security helps to improve citizens’ understanding of the importance of formalizing employment. This is exemplified by the communication policy developed by Kazakhstan’s Unified Accumulative Pension Fund. In addition, the simplification of procedures for paying contributions for very small businesses is becoming widespread. Turkey offers two examples, a “Simple Employership application” programme and the simplification of the payment of contributions for the second pillar pension. Simplified procedures can also apply to the introduction of professional standards for non-medical services associated with policies to support elders’ independent living. The French Central Agency of Social Security Bodies (Agence centrale des organismes de sécurité sociale – ACOSS) has set up services to simplify the formalization of such activity, accompanied by a tax incentive for the employed caregiver.

Good practices

France: Support for the formalization of personal services

The French Central Agency of Social Security Bodies (Agence centrale des organismes de sécurité sociale – ACOSS), which steers the Social Security and Family Allowance Collection Unions (Union de recouvrement des cotisations de sécurité sociale et d’allocations familiales – URSSAF), has implemented a policy dedicated to the formalization and professionalization of personal services. The aim is to professionalize and formalize home-help caregiving services, especially for those whose work is associated with aiding the elderly to live independently. Using the “Dematerialized universal service employment voucher” (CESU+), the process for people to formalize the home help they receive and reduce their tax bill has been simplified.

In practice, this entails a simplified online enrolment system, supported by a tax expenditure policy whereby the State bears half the cost of employing a caregiver. The aim is to ensure the professionalization of home caregiving services and to give those who work in this area formal employee status, with associated rights to professional training. Caregivers who are self-employed can pay contributions to access the right to full social protection, a process that results in micro-enterprises being formalized with their registration as single-person companies.

Source: ISSA (2022).

Azerbaijan: A social support policy for people aged 65+

Azerbaijan’s Agency for Sustainable and Operational Social Security (DOST) provides social services at home for the elderly living alone without close relatives or legal representatives. Social workers help the elderly with household chores, cleaning, food and medicine purchases, payments, and other tasks.

In addition, the Agency has developed initiatives to enhance the provision of social security for elders, including helping to improve the quality of life of the elderly and promote their active participation in society. The Agency has been designated as the executive body of the third component of a joint project on “active ageing” by the Ministry of Labour and Social Protection of Population of the Republic of Azerbaijan (MLSPP) and the United Nations Population Fund (UNFPA). Under the project, the Agency has undertaken work in several areas, such as sharing the experiences of the elderly with the younger generation, imparting new knowledge and skills about information technology to the elderly, and organizing leisure activities.

In addition, the Agency has established the “Silver DOST” programme, which employs retired people as volunteers for a minimum period of two months. The programme permits people from different backgrounds to become temporary social workers and to serve citizens at DOST service centres.

Source: ISSA (2022).

Bibliography

Bornia, L. et al. 2011. “Système migratoire et métiers du care: comment les évolutions démographiques produisent les nouvelles migrations”, in Gérontologie et Société, Vol. 34, No. 139.

Breyer, F.; Costa-Font, J.; Felder, S. 2010. “Ageing, health and health care”, in Oxford Review of Economic Policy, Vol. 26, No. 4.

Dumont, G.-F. 2020. “Les retraites en Europe: quelle perspective?”, in Les analyses de Population et avenir, December.

European Commission. 2020. Report on the impact of demographic change. Brussels.

European Commission. 2021a. Proposal for a Directive of the European Parliament and of the Council on improving working conditions in platform work (2021/0414 (COD)). Brussels.

European Commission. 2021d. 2021 Long-term care report: Trends, challenges and opportunities in an ageing society. Luxembourg, Publications Office of the European Union.

European Commission. 2021e. The 2021 ageing report : Economic & budgetary projections for the EU Member States (2019-2070) (Institutional paper, No. 148). Luxembourg, Publications Office of the European Union.

Eurostat. 2021b. Population structure and ageing. Luxembourg.

Firgo, M.; Famira-Mühlberger, U. 2020. “Öfffenliche Ausgaben für Pflege nach Abschaffung des Regresses in der stationarën Langzeitpflege”, in Monatsberiche, Vol. 93, No. 6.

Galina, A. et al. 2018. “Active Ageing Index: A Russian study”, in A. Zaidi et al., Building evidences for active ageing policies. Singapore, Palgrave Macmillan.

Gietel-Basten, S. et al. 2017. Ageing in Russia: Regional inequalities and pension reform (IEMS working paper, No. 2017-49). Hong Kong, Hong Kong University of Science and Technology – Institute for Emerging Market Studies.

ILO. 2021b. Non-standard forms of employment in selected countries in Central and Eastern Europe – A critical glance into regulation and implementation. Budapest, ILO Decent Work Technical Support Team and Country Office for Central and Eastern Europe.

ILO. 2021f. World Social Protection Report 2020–22: Social protection at the crossroads – in pursuit of a better future. Geneva, International Labour Office.

ISSA. 2022. ISSA Database of good practices. Geneva, International Social Security Association.

ISSA; SSA. 2018a. Social security programs throughout the world: Europe, 2018. Washington, DC, Social Security Administration.

ISSA; SSA. 2018b. Social security programs throughout the world: Asia and the Pacific, 2018. Washington, DC, Social Security Administration.

Muir, T. 2017. Measuring social protection for long term care (OECD Working paper, No. 93). Paris, Organisation for Economic Co-operation and Development.

Nadirova, G. 2018. “Social aspect of population aging in Eurasia”, in Weekly e-bulletin, No. 164.

OECD. 2020a. Long-term care resources and utilisation. Paris, Organisation for Economic Co-operation and Development.

OECD. 2020b. Focus on spending on long-term care. Paris, Organisation for Economic Co-operation and Development.

OECD. 2021. Pensions at a glance: OECD and the G20 indicators. Paris, Organisation for Economic Co-operation and Development.

Safonov, A.; Shkrebelo, A. 2021. Long-term care system in Russia: International benchmarks and current relevant data for the Russian Federation. Geneva, International Social Security Association.

UN. 2020. The Sustainable Development Goals report. New York, NY, United Nations.

UNDESA. 2019. World population prospects 2019. New York, NY, United Nations Department of Economic and Social Affairs.

Varlamova, M. et al. 2020. Ageing in Europe, from North to South. Brussels, European Liberal Forum.

Willemé, P.; Dumont, M. 2015. “Machines that go ‘ping’: Medical technologies and health expenditures in OECD countries”, in Health Economics, Vol. 24, No. 8.